The following article by Uri Dadush and Shimelse Ali, which was published today in the Carnegie Endowment’s International Economic Bulletin, was originally presented at a February 16th meeting of the Inter-American Dialogue’s China and Latin America Working Group.

China’s Rise and Latin America: A Global, Long-Term Perspective

Over the past decade, China has become an increasingly important economic partner for Latin America. But this trend must be placed in proper perspective. Even as trade and investment links between China and Latin America have grown, the United States and Europe are—and will continue to be—vital trading partners for the region. Moreover, China’s rise is only one part of a broader shift towards a world in which emerging markets have greater economic weight. Policymakers in Latin America need to view China’s growing influence within the context of both current economic patterns and long-term global trends.

China’s economic importance is growing, but…

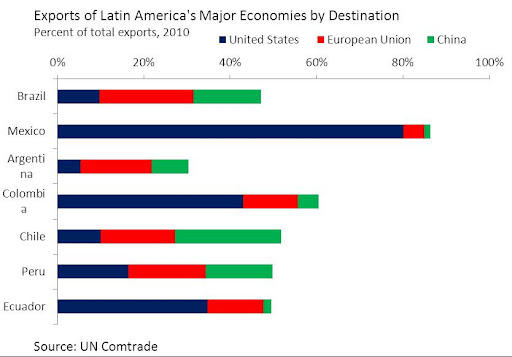

Clearly Beijing is making its mark in Latin America. In 2000, China was the seventh-largest export market for Latin America and accounted for less than 2 percent of the region’s exports. Today, China accounts for 10 percent of Latin America’s exports and is the leading export destination for Brazil and Chile. Even so, the United States and Europe remain Latin America’s most important trading partners, accounting for 40 percent and 14 percent of its exports, respectively. The United States is, moreover, a key provider of remittances to Latin America—accounting for 75 percent of the $60 billion the region received in 2008—and, thus, a critical source of foreign exchange for many countries in the region.

As the chart below suggests, there is a marked difference between China’s importance as an export market for Mexico, which is closely tied to the United States and exports manufactures that often compete with China’s, and the natural resource exporters in South America. For example, the export similarity index, a measure of the extent to which exports overlap, for China and Mexico in the U.S. market is estimated at 56.9 percent, suggesting high competition in third markets, compared to 38.5 percent for China and Brazil. China is, however, quite uniformly a more important source of Latin America’s imports than the United States.

According to the United Nations Economic Commission for Latin America, China’s foreign direct investment in Latin America reached $15.3 billion in 2010 and $22.7 billion in 2011, up from a much lower level in each of the previous nine years. Still, China is the third-largest external investor in the region, behind the United States and the Netherlands, and its share of investment trails the intraregional total.

Taking a long-term, global view

The implications of China’s rise for Latin America are best understood within a long-term, global framework. China’s emergence is only one aspect, albeit a very important one, of the ways in which the rapid rise of emerging economies is reshaping the global economy and prospects for Latin America. Already, according to projections in Juggernaut, in purchasing power parity terms, four of the seven largest global economies—Brazil, Russia, India, and China—are developing countries. Mexico will join the Big 7 by 2030 and Indonesia by 2050. By then, the United States will be the only advanced country to rank among the world’s seven largest economies. At the same time, China will become the center of world trade, representing by far the largest trading partner for most countries. Its share of world trade will reach 24 percent by 2050, up from about 10 percent today.

The rise of emerging economies other than China will create major opportunities for Latin American countries. Today, about 40 percent of Latin America’s exports go to other developing countries, including China; this figure will surge as developing countries’ share of world exports will more than double from 30 percent in 2006 to 69 percent in 2050. Moreover, the rise of regional powers Brazil and Mexico, and their burgeoning middle classes, could be a boon for other Latin American economies. In fact, Brazil already accounts for a quarter of intraregional exports.

The emergence of the developing world and weaknesses in advanced economies—the income inequality and political gridlock in the United States, the debt crisis in the Eurozone, and the fiscal and demographic crisis in Japan—will lead to a very different economic order, one in which huge new markets and new sources of competition will arise, and one in which power and influence are more widely distributed. For the first time, the world’s largest and most powerful economies will be relatively poor countries—ones whose worldviews may differ from those of advanced countries and from each other in ways that are presently difficult to discern.

Policy

China’s rise and the broader shift of the world’s economic center of gravity towards the East and the South raise at least three sets of economic policy issues for Latin America to address: comparative advantage, priorities for economic diplomacy, and the region’s role in the global system.

Comparative advantage

Contrary to the popular impression, Latin American commodity exporters cannot be sure that the rise of China and other relatively poor countries will sustain a commodity price boom forever; therefore, diversification of their economies remains a challenge.

For nearly all commodities (petroleum, where the marginal cost curve may rise steeply, could be a partial exception), increased demand may well be eventually matched by increased investments in supply and technological innovation that reduces production costs and develops new substitutes—as has happened historically. As business conditions in Russia, Indonesia, Africa, and other natural resource exporters improve, moreover, so too will their capacity to export commodities. Finally, demand for commodities will eventually be held back by the natural shift to services and manufactures as incomes rise, as well as by innovations which reduce the wastage and intensity of commodity use.

Latin American resource-based economies may sooner or later need to strengthen their capacity to produce manufactures and services, the demand for which will soar as the middle class burgeons domestically and in other emerging markets. At present, nearly 90 percent of Latin America’s exports to China are in mining and agriculture. Although the region’s terms of trade have improved, on average, by nearly 4 percent annually between 2002 and 2008, compared to 0.5 percent a year between 1995 and 2001, there is no guarantee that the recent favorable trend will persist indefinitely.

Given the profound structural changes in global demand and supply implied by the rise of the emerging powers, and the uncertainties inherent in predicting commodity prices, Latin America’s development strategy should be robust to a number of plausible scenarios. Examples of policies that could underlie such a strategy include investing in education, strengthening governance, improving the business climate, and enhancing the capacity to innovate.

Economic diplomacy

Although the relative size of the U.S. economy is expected to decline over the coming decades, the United States is projected to remain an important destination for Latin America’s exports even in 2050. Similarly, the importance of individual European economies, in terms of trade and investment, will decline over time; however, the European Union as a trading bloc is likely to be among the region’s major partners.

Thus, while Latin American countries will need to reorient their economic diplomacy towards emerging powers such as China, India, Russia, and Indonesia—including fostering trade and investment agreements—relationships with Europe and the United States will remain critical. And as Latin American economies become richer and more diversified, major opportunities are likely to arise for them to spur regional integration, especially as Brazil and Mexico are on their way to becoming two of the world’s largest economies.

Role in the global system

Latin American countries are becoming more influential on the world stage. Brazil and Mexico are already playing a prominent role in the G20, the new premier forum for global economic decision-making, of which Argentina is also a member. But as their economic power continues to grow, they will have to assume greater responsibility in shaping and contributing to the international system. These countries need to define their own vision of how the global trading system, financial regulation, migration policies, development assistance, and efforts to mitigate climate change should evolve.

Countries such as Brazil (as well as China and India) sometimes present themselves as leaders of the developing world and voices of the poor, in contrast to advanced countries. However, as developing economies become the largest and most powerful, they will be forced to seek allies among the like-minded, be they rich or poor, if they are to pursue their interests effectively.

Conclusion

China’s rise, accompanied by the rise of other emerging markets, is already providing both major opportunities and challenges for Latin America. Though China is already out-competing some countries in the region, such as Mexico in manufactures, it has created a boon, at least in the near-term, for commodity exporters and become an active investor in the region.

But China’s rise is part of a much bigger picture of a changing global economy in which emerging economies, including those in Latin America, have greater influence; a global economy that will transform in ways that are difficult to predict. One of the central lessons of development history, including the success of Asia’s initially commodity-dependent economies, is that today’s economic structure may be transient and matter less for success than the capacity to adapt to the big changes occurring at home and abroad.