Latin America’s exports of metals and ores to China boomed over the past decade as China’s growth and urbanization fueled rapid demand growth for iron ore, copper, aluminum and other commodities. Chinese consumption of metals and minerals has increased dramatically, swelling from less than 10 percent of global demand in 1990 to nearly 50 percent today and accounting for 70 to 80 percent of global demand growth over the past 10 years. Commodity exports to China have additionally fueled economic growth in Peru, Chile, and other South American nations over the past decade.

China’s GDP growth is expected to decelerate in the coming years, however, with experts projecting that the Chinese economy’s expansion will slide to around 7.5 percent in 2014 and further slow to 7.3 percent in 2015. China’s government has outlined a plan to “rebalance” the country’s economy by decreasing reliance on investment and exports and boosting consumption as a share of GDP. What impacts will slowing growth in China have for metals demand? What does this mean for Latin America’s major metals exporters? The following key trends and developments in China — as identified during the Dialogue’s China and Latin America Mining Roundtable and in a recent Dialogue report by Iacob Koch-Weser on Chinese mining activity in Latin America — will largely shape the relationship in the coming years:

Urbanization plans

China’s government plans to transition from the country’s capital-intensive and export-oriented growth path to a new growth model based on greater internal consumption and improvements in efficiency. A drop in construction during the first quarter of 2014 could indicate slowing of infrastructure investment from high levels over the past ten years, which would imply lower levels of demand for key metals such as copper and iron ore. Still, China’s Ministry of Finance announced in March that the government’s urbanization plan will provide 6.8 trillion dollars to relocate some 260 million rural citizens into China’s cities by 2020 – an expansion that will likely continue to stimulate the need for metals.

Addressing overcapacity

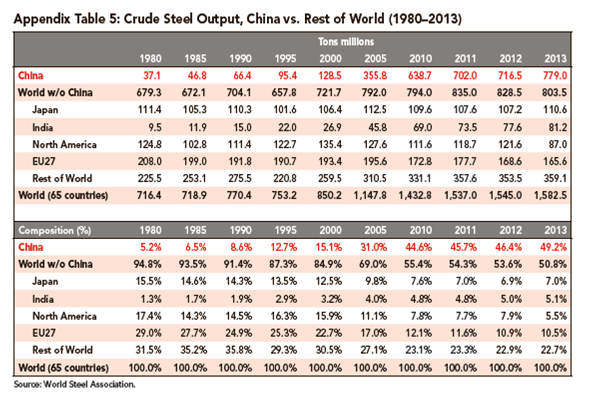

China’s vast and state-controlled steel industry, a major employer in many parts of the country, has long produced excess quantities of steel. China has been a net exporter since 2005 and currently accounts for roughly half of global production. Over the past decade, China pursued sweeping market-based reform of the country’s state-controlled firms, including fiscal and financial performance benchmarks and plans to raise the ratio of dividends to payouts, that seek to cut back surplus production by the country’s metals producers.

Yet following a period of austerity lasting through the mid 2000’s, overcapacity appears once again to be on the rise. In early 2014 the government abandoned its long-standing goal of consolidating the steel industry 60 percent by 2015, as subsequent mergers affected the balance sheets of the country’s largest firms. The financial health of Chinese mining companies – such as Baosteel, Minmetals, Wuhan and Hebei – is more precarious than ever, with evidence of decreasing operating margins, greater short-term debt exposure and lower confidence in capital markets.

Trade policy

An important component of China’s rebalancing is to decrease domestic demand for resource imports. Mining and metals play a central role in this effort. Two sets of factors exacerbate trade imbalances, and with them, excess capacity. Commodity prices, though still very high, have dropped somewhat, thereby inducing import demand. As a result, the volume of key metals imports has outpaced the value. The other factor is that China continues to use the export sector as a release valve for excess production. Particularly notable are rising net exports of steel products. Taken together, this fuels a vicious cycle of resource acquisition, commodity price inflation, and wasteful production.

Since 2004, the Chinese government’s “trade toolkit” for mining and minerals has consisted of strict import licensing, adjustments to value-added taxation (VAT), and trade tariffs. Specifically, China revoked VAT rebates for metals and minerals products, which at the time were being encouraged for export along with industrial manufactures. It soon went a step further by imposing export tariffs as well. Although this policy initially proved effective in reducing raw material exports, it has not discouraged steel and processed metals exports. Mills suffering from overcapacity are eager to reduce their inventories, even if fiscal policies are not in their favor.

Access to capital

China’s state-owned mining and metals firms have long benefited from low-interest loans issued by China’s major state-owned financial institutions. These loans have been issued domestically—through the “Big-4” banks and municipal banks—as well as internationally via China’s policy banks. Easy access to bank liquidity, combined with privileged access to capital markets and low dividend payout requirements, has provided a perverse incentive to invest in greater capacity and engage in risk-prone behavior overseas.

Recently, though, there are signs that loose credit policy is on the wane. Last July, the central bank lifted the ceiling on bank deposit rates, and in March 2014 widened the yuan’s daily trading band—bold and necessary steps toward freeing up the country’s capital accounts and exchange. In June and December of 2013, and during the first quarter of 2014, the central bank tightened its credit policy. At the 3rd Plenum in November, the Party announced that state-owned enterprises would be forced to raise their dividend payout ratio from 5 percent to 15 percent. Also in 2014, the government permitted defaults of trust loans and corporate bonds, as well as some high profile corporate bankruptcies.

How are these broader changes in financial policy impacting China’s mining and metals companies? At this point, the evidence is mixed. Among the largest miners, profligate lending continues. But in April 2014, the China Banking Regulatory Commission (CBRC) warned banks to tighten controls over letters of credit for iron ore imports. Steel mills and traders have used iron ore imports to raise money as other sources of credit dry up, as a channel for off-book or “shadow” financing. Part of the attraction of the practice is that mills benefit from lower international interest rates compared to those in China. The CBRC’s move indicates a tougher stance by the government.

Mounting environmental concerns

China’s government faces rising pressure to address to high levels of industrial pollution throughout the country. Particularly serious air pollution has a significant economic impact, with heavy smog leading to the closure of businesses and rising incidence of respiratory illnesses putting pressure on the country’s healthcare system. In December 2013, Premier Li Keqiang declared the need for a “war” on pollution, announcing plans to cut excess steel production, close certain-coal fired plants in the country and devote greater financial resources towards environmental regulation and mitigation. Still, significantly limiting pollution in the country would require a massive overhaul of industry and electricity infrastructure in a country where coal accounts for nearly 70 percent of power generation.

Although China currently leads world production of rare earth elements, growing concerns about adverse health and environmental effects have led Chinese authorities to decrease reliance on China as a primary market for these elements. China has looked at rare earths investment in Latin America and elsewhere.